A critical aspect of investing in emerging markets is the need to discriminate between short-term growth fads and sustainable development. As Paul Krugman famously discusses in his article, “The Myth of Asia’s Miracle,” it is often very easy to get caught up in aggregate GDP growth statistics without looking deeper into what is driving those statistics. This can lead to an investing-with-the-herd mentality and the systematic under-appreciation of some of the most interesting and lucrative opportunities across emerging markets.

What can we do about this? A general solution is to complete a rigorous and data-driven analysis on an industry-by-industry level. However, one useful “screener” that Krugman writes about is, instead of looking at GDP growth, charting total factor productivity growth. Total factor productivity growth essentially measures the portion of GDP growth not explained by increases in labor or capital stock. The underlying concept is that a country can achieve catch-up growth by increasing the education level of its workers or by early deployment of capital, but this growth is often unsustainable due to diminishing marginal returns. For example, a poor country may be able to increase the percentage of college-educated workers from 20% to 70% fairly quickly but the growth from 70% to 90% will be much more difficult to achieve and thus labor-driven GDP growth will slow.

Is Asian growth sustainable?

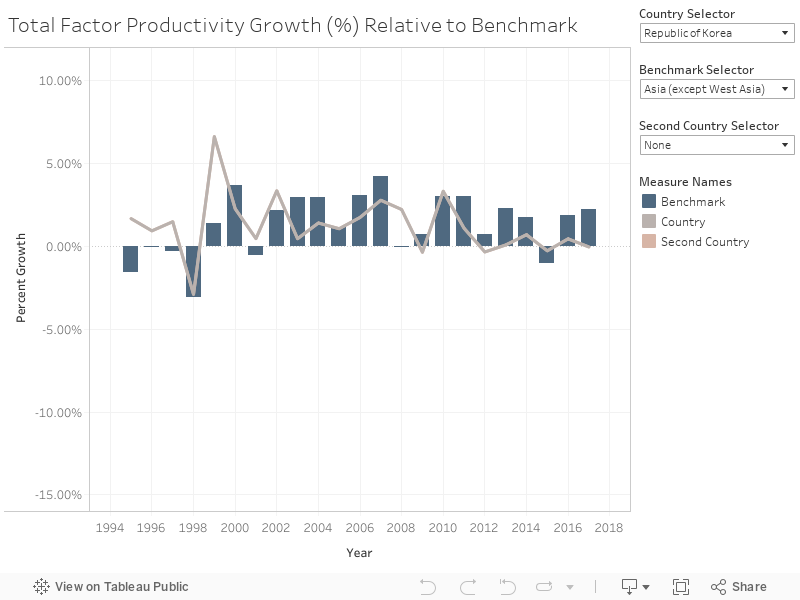

While it is recommended that one refer to Propeterra’s full country reports for deeper and more targeted analysis, it is interesting and relevant to visualize total factor productivity growth across the Asian continent. For this purpose the dynamic graph generated below is useful. In this graph one is able to visualize total factor productivity growth for up to two countries and one regional average benchmark.

Some critical points are as follows:

- Leaders in total factor productivity growth include Iran (4.7%), Mongolia (3.3%), and Kazakhstan (3.2%)

- According to this screen, these may be some of the top long-term performers. It should be noted that Iran’s productivity growth is extraordinarily volatile.

- Despite strong GDP growth levels, Chinese total factor productivity growth is actually much weaker than the world average at 0.91% relative to the global average of 1.7%

- Interestingly, productivity growth in Hong Kong is above the world average at 1.8%

- Significant underperformers include Sri Lanka (-.7%), Korea (-0.0%), and Singapore (.1%)

How do these numbers compare with actual future GDP growth rates?

While short-term and anecdotal, it is worth noting that Singapore, China, and Korea showed a slowdown in GDP growth into late 2018. In contrast, Mongolia showed strong GDP growth acceleration and Kazakhstan GDP growth remained mostly stationary from 2017 to 2018. This suggests support for the importance of total factor productivity growth. For a full econometric analysis, however, see our proprietary report on the causative relationship between total factor productivity and sustained GDP growth rates.